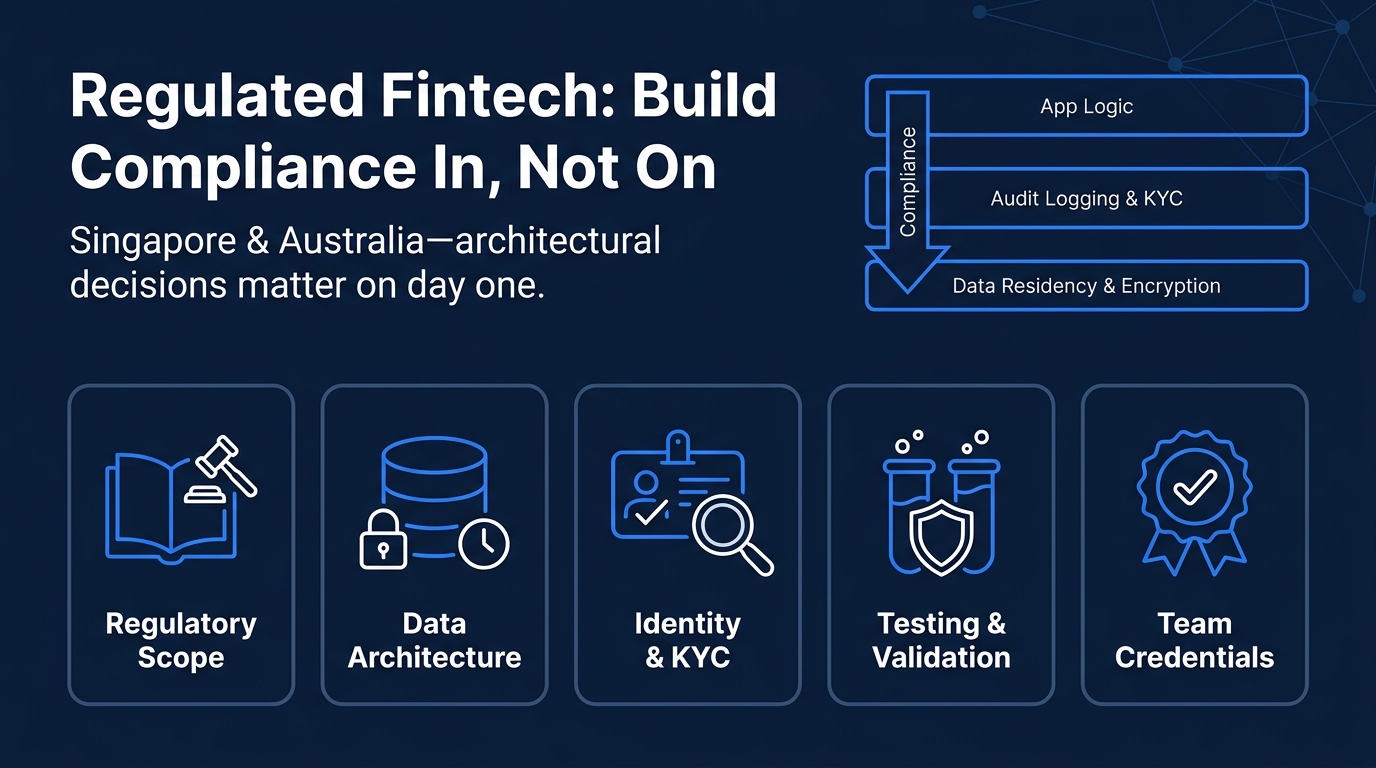

If you are shipping a fintech product into Singapore or Australia with an offshore Vietnam software team, compliance is not a phase you add at the end. It is an architectural decision made on day one. Teams that treat regulatory requirements as a checklist typically rebuild core modules six to twelve months in. The teams that succeed embed compliance thinking into every sprint from the start.

TL;DR

- Singapore (MAS) and Australia (ASIC/APRA) have distinct licensing regimes; your engineers need to understand which one applies to your product before writing a line of code.

- Data residency, encryption standards, and audit logging are non-negotiable technical requirements, not optional add-ons.

- Regulatory sandboxes in both markets exist specifically to help early-stage fintech products test before full licensing.

- A Vietnam software team with fintech delivery experience and ISO 27001:2022 / SOC 2 Type II credentials closes most of the trust gap with regulators and enterprise clients.

- Build compliance into your architecture, not your deployment checklist.

About the Author: 724SOFTWARE is a Vietnam-based technology partner with hands-on delivery experience in regulated fintech products, including capital markets platforms, crypto investment tools, and ISO 8583 card-processing systems built for Hong Kong, Singapore, and global clients.

What regulatory frameworks actually govern fintech in Singapore and Australia?

Regulatory clarity is the first technical input your development team needs, not a legal afterthought. The frameworks in Singapore and Australia differ in structure, and confusing them creates costly rework.

Singapore (MAS)

The Monetary Authority of Singapore is both the central bank and financial regulator. Key instruments your team should know:

Payment Services Act (PSA): Covers digital payment tokens, e-money, and domestic / cross-border money transfer. Most consumer fintech products fall here.

Securities and Futures Act (SFA): Governs investment platforms, robo-advisors, and digital asset products framed as securities.

MAS Technology Risk Management (TRM) Guidelines: These are not soft suggestions. They prescribe specific controls for system resilience, access management, and penetration testing cadence.

Australia (ASIC / APRA)

Australia splits prudential and market regulation across two bodies:

ASIC holds Australian Financial Services Licences (AFSL) and governs consumer-facing financial products.

APRA regulates deposit-taking, insurance, and payments infrastructure under CPS 234 (information security).

The Consumer Data Right (CDR) regime applies to open banking integrations and imposes strict data-sharing standards.

Dimension | Singapore (MAS) | Australia (ASIC/APRA)

|

|---|---|---|

Primary licence | Payment Services Act / SFA | AFSL / ADI licence |

Data security standard | MAS TRM Guidelines | CPS 234 (APRA) |

Open banking | SGFinDex | Consumer Data Right (CDR) |

Sandbox available | MAS Sandbox | ASIC Innovation Hub |

Crypto regulation | Digital Payment Token (DPT) | AUSTRAC (AML/CTF) |

What does "compliance by design" actually mean for your engineering team?

Compliance by design means the decisions that satisfy regulators are made at the architecture and data-model level, not patched in during a security audit. The following are the non-negotiable technical requirements your Vietnam software team needs to implement from sprint one.

1. Data residency and sovereignty

- MAS and APRA both have guidance on where customer financial data can be stored and processed.

- Cloud infrastructure decisions (region selection in AWS, GCP, or Azure) must reflect this before your first deployment.

- Connecting a Vietnamese development environment to production data requires documented access controls and VPN policies.

2. Audit logging

- Every state change to a financial record must be logged with a timestamp, user ID, and prior value.

- Logs must be immutable and retained for periods specified by the regulator (typically five to seven years).

- Build this into your data model early; retrofitting immutable audit trails into a live schema is expensive.

3. Encryption standards

- Data at rest: AES-256 minimum.

- Data in transit: TLS 1.2 or higher; TLS 1.0/1.1 explicitly deprecated under MAS TRM.

- Key management must be documented and reviewed, not left to default cloud settings.

4. Identity, KYC, and AML hooks

- Your onboarding flow must support eKYC integration (document OCR, liveness detection, sanctions screening).

- Design your user model to carry KYC status as a first-class field, not a flag bolted on later.

- AML transaction monitoring requires event-driven architecture; batch jobs are insufficient for real-time screening.

5. Penetration testing and VAPT

- MAS TRM requires Vulnerability Assessment and Penetration Testing (VAPT) at defined intervals.

- Build testable environments that mirror production; pen tests against a watered-down staging environment satisfy nobody.

Should you use a regulatory sandbox, and how does it change your build?

A regulatory sandbox lets your product operate under relaxed licensing conditions for a defined period while you validate the business model and demonstrate controls to the regulator. Both MAS and ASIC run formal sandbox programs.

Using a sandbox does not mean compliance requirements disappear. It means the regulator is watching your build more closely than normal, which has direct engineering implications:

Reporting cadence: Sandboxes typically require monthly or quarterly reporting to the regulator. Build internal dashboards that surface the data they ask for (transaction volumes, error rates, incident logs) before you need them.

Scope boundaries: Sandboxes cap transaction volumes or user counts. Your system must monitor and restrict these limits technically, not just contractually.

Exit criteria: Graduating from sandbox to full licence requires demonstrating that production controls are in place. Treat sandbox phase as a proof run for your compliance architecture, not a permission to skip it.

Vietnam's own regulatory sandbox experience with fintech is evolving rapidly, which means engineers working from Vietnam have growing domestic context for what sandbox-era compliance actually looks like in practice.

What your Vietnam software team needs in place before the first commit

Building a regulated fintech product is not about hiring more lawyers; it is about engineering discipline applied to the right problems from day one. Here is a practical checklist:

Regulatory scope confirmed: which licence type applies (PSA, AFSL, DPT, etc.)

Cloud region locked to compliant data residency zones

Secrets management configured (no credentials in source control)

Audit log schema defined in the data model

Encryption standards documented and enforced at the infrastructure layer

KYC/AML provider selected and API contract drafted

VAPT cadence agreed and test environment provisioned

Incident response runbook written (who is notified, within what timeframe)

A Vietnam software team operating under ISO 27001:2022 and SOC 2 Type II certification arrives at this checklist with most of the internal controls already in place. The certification does not replace regulatory compliance, but it demonstrates to auditors and enterprise clients that the delivery process itself is controlled.

Frequently Asked Questions

Can a Vietnam-based team legally access production data for a Singapore or Australian fintech product?

Yes, but with documented controls: role-based access, VPN enforcement, access logs, and data processing agreements aligned to the applicable privacy law (PDPA in Singapore, Privacy Act in Australia).

What is the difference between MAS TRM Guidelines and ISO 27001?

ISO 27001 is an internationally recognised information security management standard. MAS TRM is Singapore-specific and prescribes more granular controls for financial institutions. Holding ISO 27001 is a strong baseline; it does not automatically satisfy MAS TRM, but significantly reduces the gap.

When should compliance architecture decisions be made?

Before your data model is finalised. Audit logging and encryption are schema-level decisions. Retrofitting them costs significantly more than building them in from the start.

Does using a regulatory sandbox reduce development requirements?

No. It reduces licensing requirements temporarily. The underlying technical controls (encryption, logging, KYC hooks) must still be present because the regulator is actively reviewing your build during the sandbox period.

How long does MAS or ASIC licensing typically take?

Duration depends on licence type and completeness of your application. The sandbox route is specifically designed to reduce time-to-market while licensing is in progress.

What certifications should I look for in an offshore fintech development partner?

ISO 27001:2022 (information security), SOC 2 Type II (operational controls), and GDPR compliance are the minimum credible baseline for a regulated product. Ask specifically for the 2022 version of ISO 27001, as the original 2013 standard has been superseded.

Is Vietnam a viable delivery location for regulated fintech work?

Vietnam has a growing track record in fintech delivery and its own evolving regulatory sandbox framework. Teams based there are actively building regulated products for Singapore, Hong Kong, and Australian markets today.

About 724SOFTWARE

724SOFTWARE is a Vietnam-based technology partner with 200+ professionals, 58% of whom are senior-level engineers, delivering fintech, healthcare, and enterprise software products across 10+ countries. The company holds ISO 9001, ISO 27001:2022, SOC 2 Type II, and GDPR compliance, and is an official partner with Claude (Anthropic) and Cursor. With a 95% client retention rate and a track record spanning capital markets platforms, ISO 8583 card processing, and crypto investment tools, 724SOFTWARE works with clients as a long-term technology partner, not a one-off delivery shop.

Ready to build a regulated fintech product with a team that already understands the compliance architecture? Visit 724SOFTWARE to start the conversation.